Insolvency proceedings are a legal process that allows a company or self-employed person in a situation of insolvency to protect and reorganize itself in order to achieve business continuity. However, these processes can have important consequences in the operation of VAT by companies. Learn about some of the mechanisms to recover VAT in these situations and avoid possible tax losses, read on!

What is an insolvency proceeding?

It is a legal process that takes place when a company or individual is unable to meet its debts. During this process, the insolvency and lack of liquidity of a business is evaluated, and a plan is developed to distribute the available resources among creditors in an equitable manner.

The objective is to enable the company or individual to reorganize and continue operations. In other words, to avoid bankruptcy or to achieve a fair and effective resolution for all parties involved.

This insolvency proceeding may be directed towards a self-employed person, a legal entity or individual, large companies or SMEs. Even so, most of the insolvency proceedings in Spain are requested by companies.

It is, therefore, a system to help companies and self-employed professionals in insolvency situations to manage their debts in an orderly manner.

By filing for insolvency proceedings, responsibility rests with a judge and debt foreclosures can be stopped or a reduction and deferral of payment can be negotiated. Law 22/2003, of July 9, 2003, which supports bankruptcy, seeks to preserve the company and its assets rather than dissolve it completely.

The partner’s equity is used as collateral and is the last to receive payment of the debt.

You may also be interested in: VAT rates in Spain: updates 2022

How do insolvency proceedings affect companies’ VAT?

In an uncertain economic environment, it is important to know how insolvency proceedings affect companies’ Value Added Tax (VAT).

The insolvency law regulates the insolvency situation of a company, but it can also have VAT implications. Taking into account the two possible scenarios that may exist in any insolvency proceeding, we explain the VAT implications and ways to recover debts.

Scenario 1: you are a bankrupt company

In the case of a company that has been declared bankrupt, its debts are classified into two categories: bankruptcy claims and claims against the mass.

Claims on the first debt are suspended and it is common for creditors, including the Treasury, to receive only a portion of the total. In the case of the second debt, claims are not suspended.

The deal that must be struck for the bankruptcy to be successful is complicated to apply to the VAT return during the period in which the bankruptcy takes place. Since it will include both pre-bankruptcy and post-bankruptcy VAT dues.

In this case, it is difficult to determine whether the result (to be paid or to be offset) has the character of a bankruptcy claim or a claim against the insolvency estate.

To address this situation, two VAT returns must be filed in the period in which the order of admission to insolvency proceedings is issued.

The first corresponds to transactions carried out before the date of the order (pre-bankruptcy period). The other corresponds to the operations carried out after (post-bankruptcy period).

If there is an accumulated balance to be offset from previous periods, it must be applied first in the pre-bankruptcy return and, if there is an excess, in the post-bankruptcy return.

You may also be interested in: What is the Financial Transaction Tax?

Scenario 2: your customer is a bankrupt company

In the current crisis, many companies are forced to file for bankruptcy due to insolvency in order to continue their business.

In these cases, many of their creditors seek VAT recovery. Companies and self-employed workers enter into a state of uncertainty about the real possibilities of recovering the tax if a client files for bankruptcy.

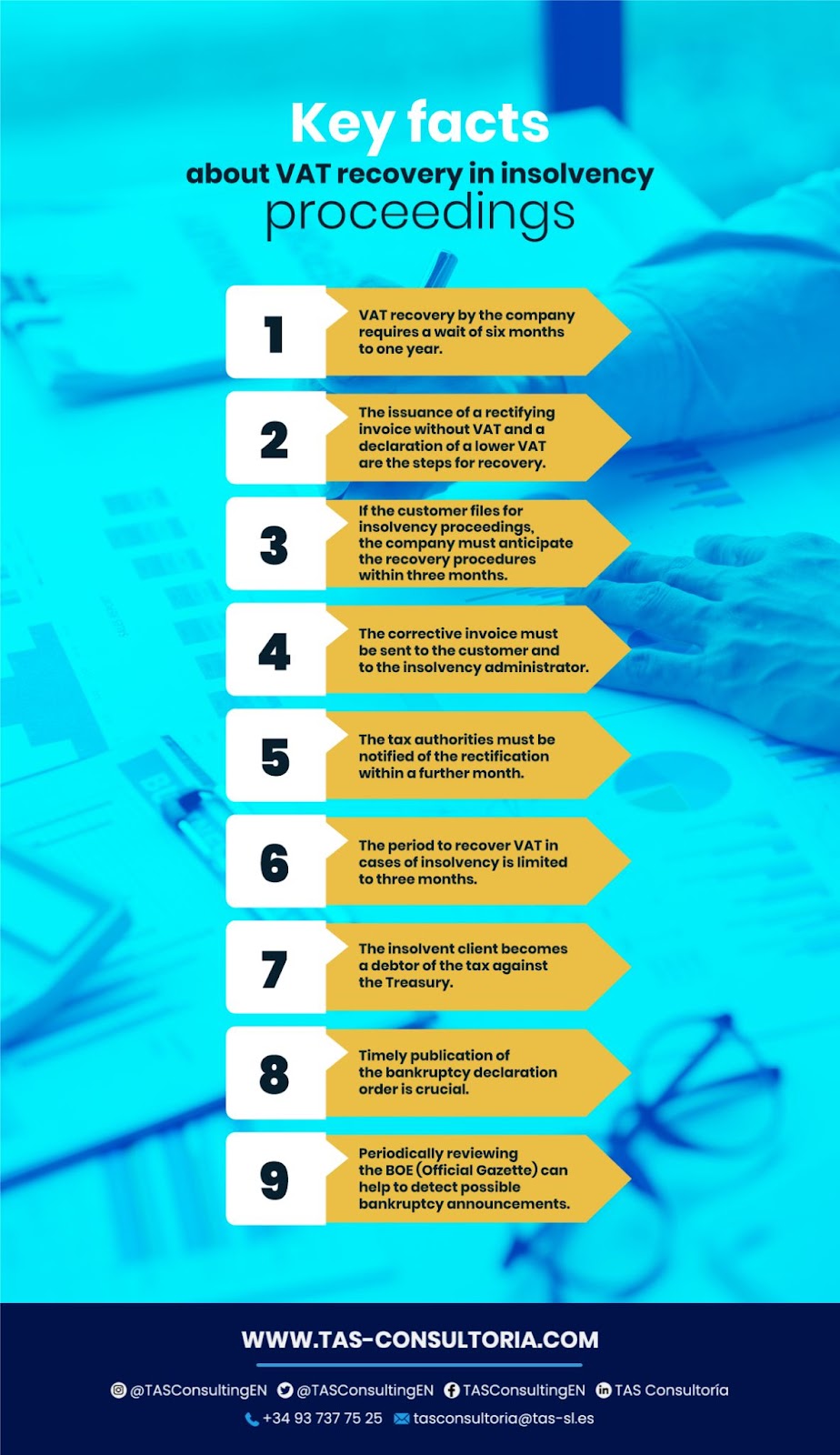

Companies with outstanding invoices from a customer in insolvency proceedings can recover the VAT on these invoices by modifying the taxable base.

The recovery of VAT by the company means that the insolvent customer becomes a VAT debtor vis-à-vis the tax authorities. This is because it has to account for less input VAT in its returns.

The problem lies in knowing in a timely manner the publication of the bankruptcy order. The insolvency administrator must notify the creditors, but there may be delays.

Therefore, it is advisable to periodically review the BOE to detect possible announcements of contests. This professional firm is available to help with any questions or concerns you may have.

Insolvency proceedings can have serious consequences on the company’s VAT. It is important to be attentive and act in a timely manner to recover the tax charged and avoid unexpected surprises.

You may also be interested in: How can you register for Social Security?

Tax management in special situations, as we have explained in both scenarios, requires in-depth knowledge and experience in the tax field.

Do not hesitate to contact us if you need help or advice regarding an insolvency situation. We offer you a personalized and efficient service, with the aim of minimizing the fiscal impact of unforeseen events. Do not wait any longer to protect your fiscal interests and leave your management in our hands!

Your email address will not be published .

Required fields are marked with *