Are you a non-resident who wants to buy or sell your property in Spain? Well, it is important to mention that this is subject to Non-Resident Income Tax (IRNR). The difference between the transfer and acquisition values will determine the gain. Do you want to understand better how this process works? Then, the first step is to stay in our article until the end, join us!

What is the process of buying and selling a property?

The purchase and sale of a property consists of a contract by which a seller transfers his property to a buyer for an agreed price. This contract must be formalized with a public deed before a notary and then in the Land Registry.

The Civil Code and other specific rules regulate the sale and purchase of real estate in Spain. For example, the type of real estate, the form of payment, the conditions of the transfer, etc. So, the most important aspects that you must take into account as a non-resident are:

We can say, then, that the purchase and sale of real estate in Spain is a complex operation. It requires professional advice and proper planning by each of the parties. For that reason, we recommend you to count on the help of a lawyer, a manager or a real estate agent to guide you and facilitate the necessary procedures.

You may also be interested in: The lease contract for commercial premises in Spain

Where is the purchase and sale of a property by a NON-resident taxed?

The non-resident buyer must withhold and pay 3% of the agreed consideration to the Treasury. This withholding is considered by the seller as a payment on account of the tax. Remember that this corresponds to the gain derived from the transfer.

Likewise, if the taxpayer is a non-resident in Spain and is the owner of real estate, he/she will be subject to IRNR. Thus, the capital gain as a consequence of the sale of a property is taxable income.

The purchase and sale of real estate is a transaction that generates tax obligations for both the seller and the buyer. However, these obligations vary according to the tax residence of the parties involved.

Therefore, the first thing to do is to distinguish between VAT and Transfer Tax and Stamp Duty (ITP and AJD).

In the case of VAT, since it is a direct tax, it is levied on the consumption of goods and services. While ITP and AJD are direct taxes levied on the transfer of goods and rights. However, when the buyer is a non-resident, some particularities must be considered:

- If the seller is a Spanish resident, 3% of the sale price must be withheld and paid to the tax authorities. This will be the payment on account of the non-resident income tax payable by the buyer.

- This withholding must be made with Form 211 and is presented within one month from the date of the public deeds.

- If the purchaser is not satisfied with the withholding tax withheld, he may request a refund or offset against the corresponding non-resident income tax.

You may also be interested in: Taxes in Spain for foreigners

What is Non-Resident Income Tax?

The Non-Resident Income Tax (IRNR) is a tax levied on income obtained in Spanish territory by individuals or entities not resident in Spain. This tax applies to income from work, from movable or real estate capital, from economic activities, among others.

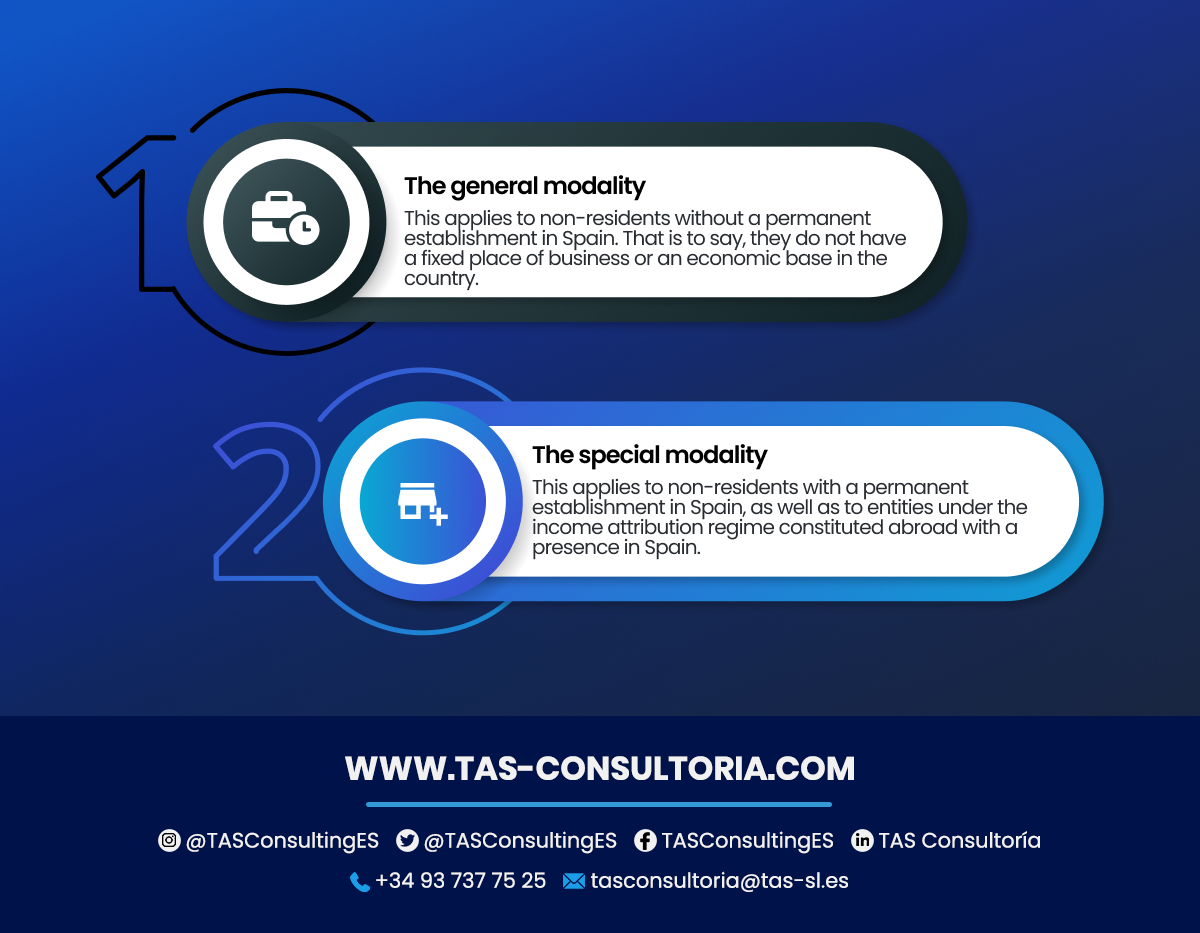

The IRNR is regulated by Law 41/1998, of December 9, 1998, and by Royal Decree 1776/2004, of July 30, 2004, which approves the tax regulations and has two modalities:

This IRNR is declared and paid by means of forms 210, 211 and 216, as the case may be. The deadline for filing the return varies according to the type of income and the way it is obtained. In general, the deadline is quarterly or annual, with some exceptions.

It is a complex tax that requires a good knowledge of the Spanish regulations and those of the countries of origin and residence of the taxpayers. Therefore, it is recommended to consult a specialized advisor before carrying out any operation that generates income subject to IRNR.

What is the Transfer Tax and Stamp Duty?

The ITP and AJD is a tax levied on the purchase and sale of real estate. Likewise, it also taxes the formalization of notarial, mercantile and administrative documents in Spain.

This being so, this tax applies to both onerous property transfers (TPO). That is to say, those that involve an economic consideration, such as corporate transactions and documented legal acts.

In this sense, the ITO and AJD is a tax ceded to the autonomous communities. This means that each one can establish its own tax rates and bonuses. Therefore, the amount to be paid may vary depending on the region where the transaction is made.

In addition, the tax is calculated on the real value of the property or right transferred and not on the price agreed between the parties. This tax must be paid within 30 working days following the date on which the contract or public document is formalized.

Likewise, in order to settle the tax, form 600 or form 620, as the case may be, must be filed with the corresponding tax office.

You may also be interested in: Hiring a real estate agency: what should you know?

Did you buy a property and need to pay the Income Tax for Non Residents? We invite you to contact our professionals through our email tasconsultoria@tas-sl.es. Our team of managers and advisors will provide you with the necessary help based on your needs. What are you waiting for? Schedule your personalized advice.

Your email address will not be published .

Required fields are marked with *